Ian Harnett in Financial Times: The AI capex endgame is approaching

- Absolute Strategy

- Oct 3, 2025

- 3 min read

The writer is co-founder and chief investment strategist at Absolute Strategy Research

The AI “bubble” looks to be approaching its endgame. The dramatic rise in AI capital expenditure by so-called hyperscalers of the technology and the stock concentration in US equities are classic peak bubble signals. But history shows that a bust triggered by this over-investment may hold the key to the positive long-run potential of AI.

AI stocks have exhibited bubble characteristics for a while. Share prices have skyrocketed, driving excessive index concentration. AI companies are doing deals between themselves, helping inflate their valuations. And they are buying each other’s products and using vendor financing to sustain growth.

Until recently, the missing ingredient was the rapid build-out of physical capital. This is now firmly in place, echoing the capex boom seen in the late-1990s bubble in telecommunications, media and technology stocks. That scaling of the internet and mobile telephony was central to sustaining “blue sky” earnings expectations and extreme valuations, but it also led to the TMT bust.

This followed the similar patterns from the introduction of nearly all general-purpose technologies — from railways, electricity, radio, semiconductors, to the internet. These bubbles didn’t end because the dream about the new technologies fell short; rather, the bubbles burst either due to regulation, increased competition, or the buyers of the products being unwilling, or unable, to sustain the demand. While the technology theme may be structural, all too often the end users are cyclical, putting the returns on investment in this excess capacity at risk from weakness in end-user cash flow.

Today’s AI hyperscalers are seeing these vulnerabilities emerge. Europe is leading the way on regulation, with the European AI Act. Competing models Deep Seek from China and K2 from the United Arab Emirates use less computing power. More importantly, tech cash-flows are beginning to be squeezed. If the end buyers of AI suffer an exogenous cash flow shock, the merry-go-round will slow rapidly as sales collapse faster than capex can be reined in, resulting in faltering earnings and accelerated cash burn. Tech buybacks would also likely be cut, undermining both share prices and market valuations.

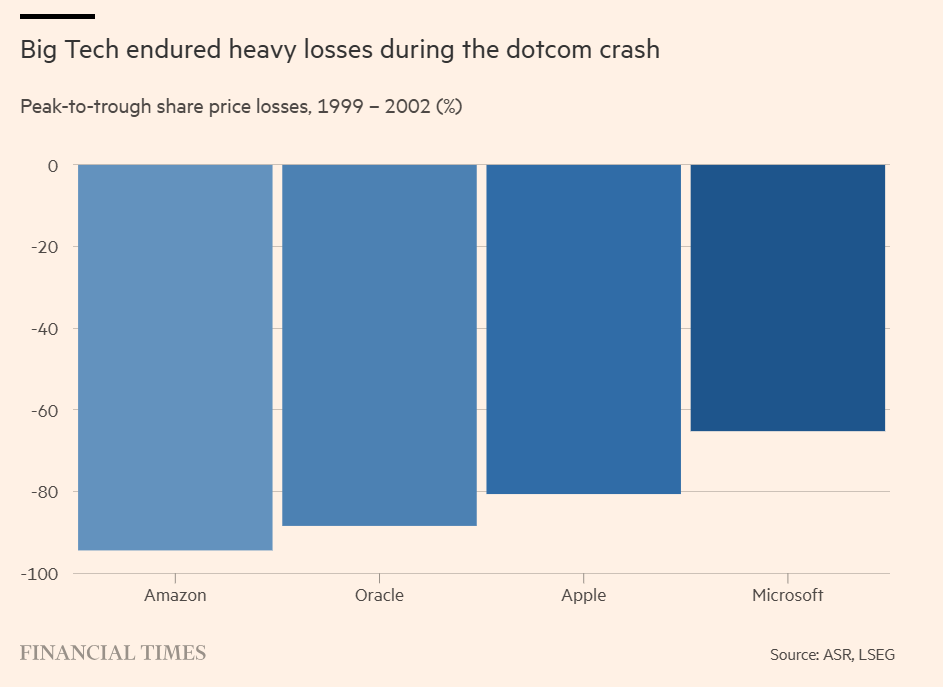

So the message for today’s investors is “buyer beware”. The TMT bust shows why. Today we are living the digital dream envisioned in the TMT bubble: a hyperconnected world, with seamless digital communication and where the internet of things is a reality. Yet this did not stop today’s digital winners from the TMT era falling heavily in the tech bust — Microsoft (65 per cent), Apple (80 per cent), Oracle (88 per cent), and Amazon (94 per cent). These companies took 16, five, 14 and seven years respectively to regain their 2000 peaks.

My perspective on technology bubbles has been shaped by four themes that emerged from William Janeway’s book Doing Capitalism in the Innovation Economy. First, periods of bubble behaviour — and especially excess capex — are central to the adoption of new technologies. The hype around them drives down the cost of capital, allowing the rapid build-out of the new technology.

Second, when the bubble bursts, the excess capacity does not just disappear. It can be acquired at low prices by new players. The waste in the creative destruction identified by economist Joseph Schumpeter is inherent to bubbles, giving access to the new technology capacity at a lower price than if the boom persisted. This cheap capacity helps embed the technology in society.

My perspective on technology bubbles has been shaped by four themes that emerged from William Janeway’s book Doing Capitalism in the Innovation Economy. First, periods of bubble behaviour — and especially excess capex — are central to the adoption of new technologies. The hype around them drives down the cost of capital, allowing the rapid build-out of the new technology. Second, when the bubble bursts, the excess capacity does not just disappear. It can be acquired at low prices by new players. The waste in the creative destruction identified by economist Joseph Schumpeter is inherent to bubbles, giving access to the new technology capacity at a lower price than if the boom persisted. This cheap capacity helps embed the technology in society.

Read further here: The AI capex endgame is approaching